English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Based on everything discussed in the previous review, it seems we're witnessing an emerging tug-of-war between Donald Trump and the Swiss National Bank (SNB). The SNB wants a weaker franc, and Trump wants a weaker dollar. If Trump perceives the SNB's actions as "interventions aimed at making Swiss goods more competitive abroad," the likely response would be new tariffs or sanctions. This week, the U.S. Treasury and the Swiss National Bank released a joint statement declaring that neither side is engaging in currency manipulation to gain a competitive advantage. Based on this, both parties may maintain a neutral stance moving forward.

The SNB could allow the USD/CHF exchange rate to float freely and instead focus on stabilizing the EUR/CHF pair. However, tensions between Bern and Washington are being further exacerbated by Trump's new sector-specific tariffs on pharmaceutical imports. Pharmaceuticals are a critical—and arguably the most important—component of Swiss exports. Now, Swiss medicines sold in the U.S. will cost twice as much due to these new tariffs. It seems inevitable that demand will start to decline after October 1.

Given the SNB's decision to reduce exposure to the U.S. dollar, other global central banks may begin transitioning toward alternative reserve and trading currencies. Switzerland's monetary authorities have signaled to the world which direction they intend to take in the coming years, giving other central banks tacit approval to follow suit. Additionally, nearly a quarter of the SNB's reserves are invested in U.S. tech stocks. Should Switzerland begin offloading dollars, significant sell-offs in American equities could follow. For the U.S. stock market, this wouldn't necessarily be catastrophic—other investors are likely to quickly absorb the supply. However, it could lead to increased market volatility in the short term.

All things considered, Donald Trump's protectionist policies are clearly influencing how other nations and central banks position themselves. Just a few months ago, I predicted that many consumers, corporations, and even governments might quietly begin rejecting U.S. goods, services, or cooperation with the White House, as long as Trump remains in power. No one likes being dictated to or seeing the rules of fair and competitive trade being bent or broken.

Wave Structure for EUR/USD:

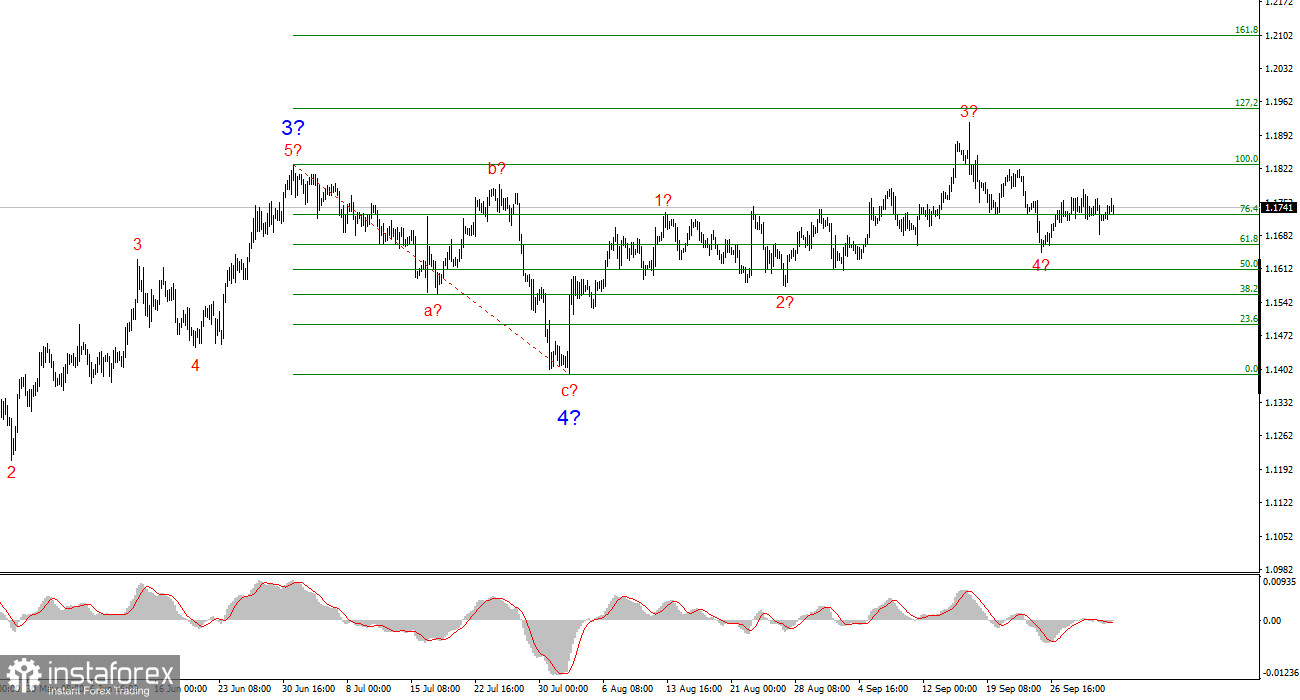

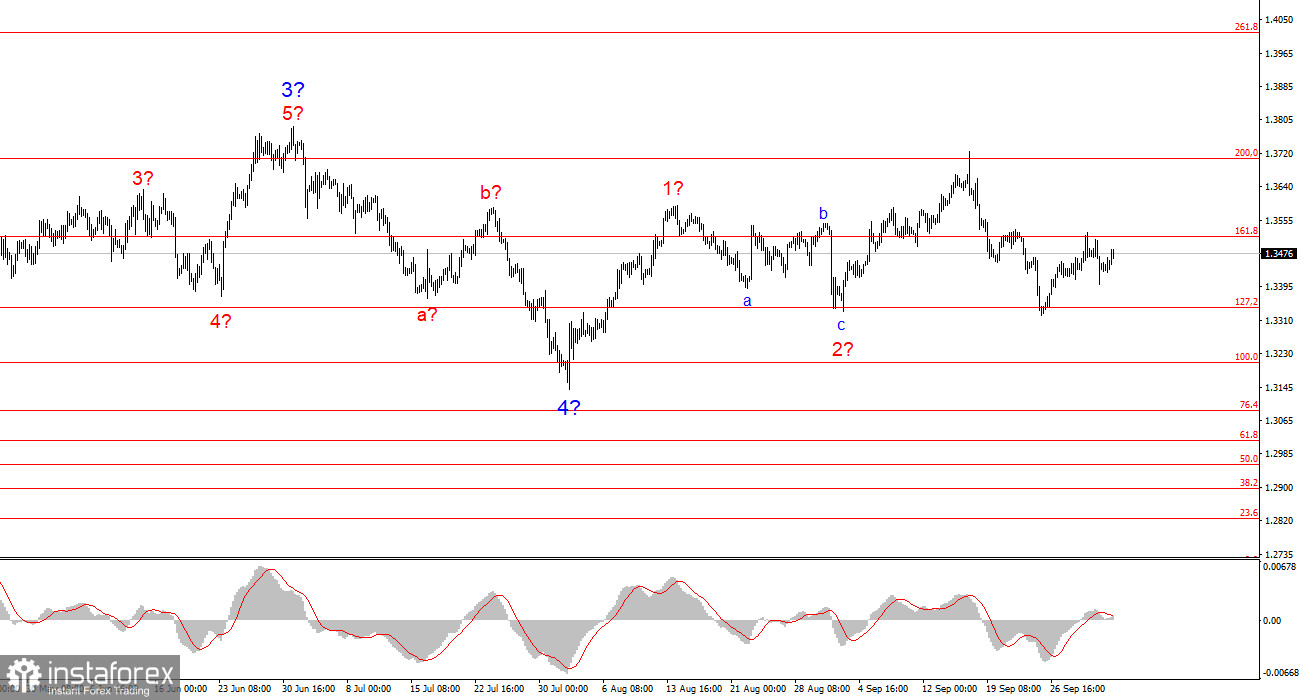

Based on the analysis, EUR/USD continues to build a bullish trend segment. Wave structure still heavily depends on news flow, Trump's decisions, and geopolitical dynamics within the White House. The current trend phase may extend all the way to the 1.2500 level. At present, a corrective wave 4 appears to be forming—or already completed. The bullish wave structure remains valid, and therefore, I am looking only for buying opportunities in the near term. By year-end, I expect EUR/USD to reach 1.2245, which corresponds to the 200.0% Fibonacci.

Wave Structure for GBP/USD:

The wave pattern for GBP/USD has evolved. We are still within an impulsive upward segment, but its internal structure has become unreadable. If wave 4 turns out to be a complex, three-wave formation, it will balance the structure—but it may also be significantly larger and longer than wave 2. In my opinion, the best reference level is 1.3341, which aligns with the 127.2% Fibonacci. Two failed breakouts of this level indicated that the market was poised for new buying opportunities. Price targets are still above the 1.3800 level.

Core Principles of My Analysis:

- Wave structures should be simple and clear. Complex structures are hard to trade and are often subject to change.

- If there is no confidence in market direction, it's better to stay out altogether.

- You can never be 100% sure of directional moves. Don't forget to use stop-loss orders.

- Wave analysis can be (and should be) combined with other types of analysis and trading strategies.