English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Canada's trade deficit widened significantly in August, reaching 6.3 billion CAD compared to 3.8 billion CAD in July. The key factor behind this shift was the implementation of new tariffs, which led to a noticeable decline in exports to the United States. Weakened exports are expected to put pressure on GDP growth in the third quarter, which already looks uncertain after the disappointing second-quarter contraction of -0.4%. The likelihood of a rebound now appears low.

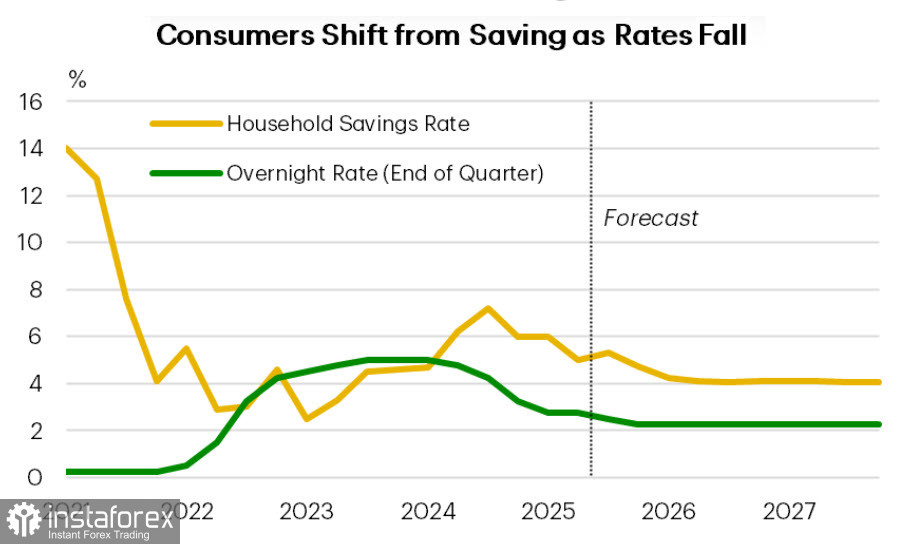

Consumer demand in Canada is rising, primarily due to the Bank of Canada's rate cuts, which have encouraged household spending. Not even the threat of higher prices from new U.S. tariffs deterred Canadian consumers—household spending in Q2 rose by 4.5%. However, this surge remains insufficient to signal a robust recovery. Consumer spending is projected to grow at a monthly rate of just 1.3–1.4% through year-end, which is below the trend level. As consumption increases, the savings rate is falling, which, combined with still-high unemployment, may pose a risk to demand in the near future.

The situation remains challenging for the Bank of Canada. Although the interest rate has been reduced from its peak of 5.00% to 2.75%, the accompanying boost to economic activity and household consumption has not been strong enough to shift the economy into sustained growth.

On Wednesday, Prime Minister Mark Carney headed to Washington, where trade relations between the U.S. and Canada will be at the top of the agenda. Whether he returns with positive outcomes remains to be seen. For now, it must be assumed that even the current 2.75% rate is not enough to support the economy.

The Bank of Canada's next meeting is scheduled for October 29, and another rate cut is widely expected. On Friday, Canada's labor market report will be released. Forecasts indicate a negative outcome, with unemployment projected to rise to 7.2% and a net loss of 50,000 jobs. All indicators suggest that the Bank should continue cutting rates. The only obstacle to further easing could be inflationary risks.

So far, signs of price pressure remain subdued. However, inflation is expected to rise in the U.S., UK, Australia, and New Zealand, and whether Canada can avoid this global trend will become clearer with the inflation report due on October 21.

In general, the Canadian economy remains too weak to assume that the Bank of Canada will conclude its rate-cutting cycle in October. As a result, pressure on the loonie is likely to grow, especially when factoring in the U.S. Federal Reserve's dovish stance on future rate moves.

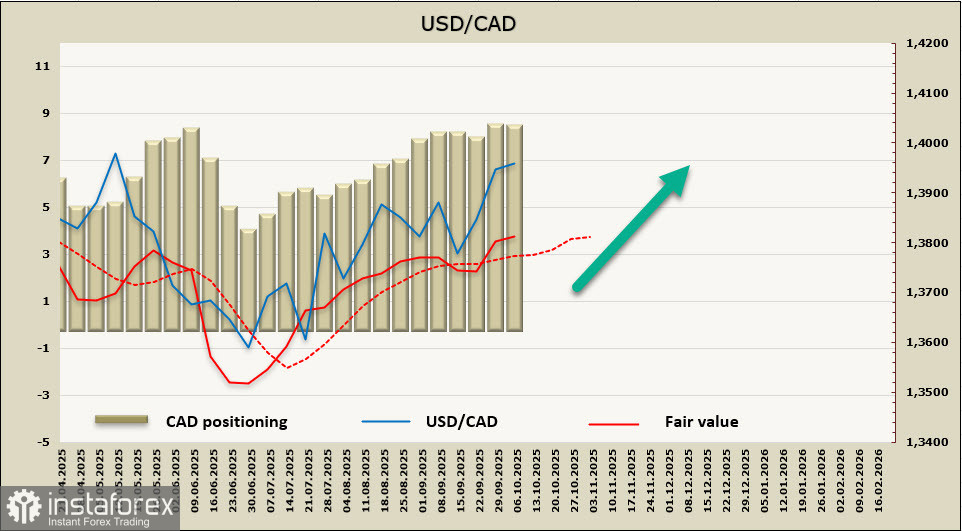

The calculated fair price remains above the long-term average, supporting the view that there is continued upside.

As expected, the USD/CAD pair has climbed somewhat higher, nearly reaching the resistance zone at 1.4010/30, where the upper edge of the channel is located. The middle of the channel, at 1.3905/20, serves as near-term support and could act as a target for a technical pullback. However, there is currently no strong fundamental reason for a deeper drop toward the lower band near 1.3780/3800.

We expect the pair to resume its upward movement after forming a new base.