English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

The European Central Bank, as expected, kept interest rates unchanged at its meeting last week. No new forecasts were presented, so the main criterion for interest rate forecasting —namely, the inflation forecast —remains the same. ECB President Lagarde noted a decrease in several risks to the economy, and the tone of the accompanying statement is assessed as neutral, with the interest rate forecast remaining unchanged—the ECB has completed its easing cycle and will not change the rate at least until the middle of next year.

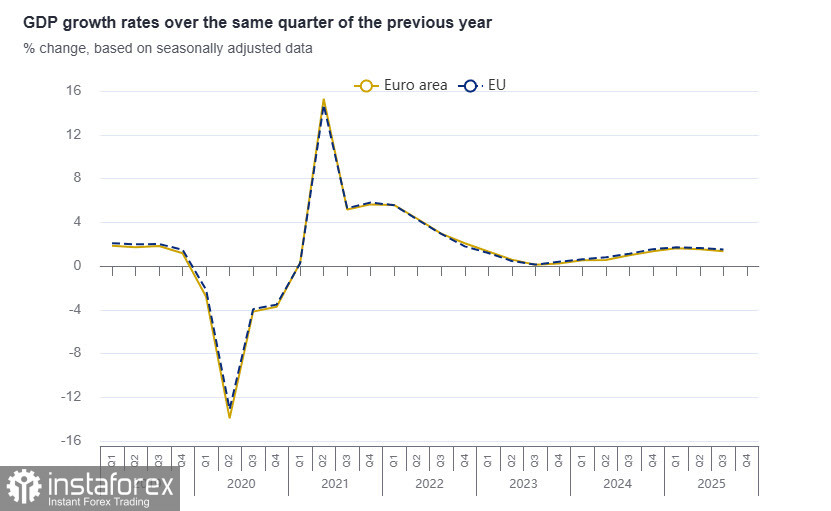

Immediately before the meeting, a report on Q3 GDP was published, showing better-than-expected results. Since the ECB had anticipated zero growth in September, the positive outcome was a pleasant surprise that further lowered expectations of interest rate hikes—the economy is strong enough to refrain from hasty stimulus measures.

October inflation in the Eurozone was slightly above expectations but within the ECB's forecasts and did not support the euro. The decline in overall inflation was driven by food and energy prices, while prices in the services sector rose; the overall picture remains neutral.

The shutdown in the US continues, meaning there will be no employment data published on Friday. Investors will have to rely on other data, specifically the ADP and ISM reports, to assess the state of the US economy. The shutdown currently acts as a bullish factor for the dollar, as the lack of reliable data increases risks, and the Fed may forgo its planned rate cut in December. In any case, comments from Fed officials following the last meeting do not indicate consensus—Waller advocates for a rate cut in December, Bostic agreed with Powell that a cut in December is "by no means a foregone conclusion," while Harker and Logan clearly stated that they do not see the need to lower rates. At present, the market expects rates to be cut, but everything points to an increasing likelihood that they will remain at current levels, which is decidedly bullish for the dollar.

The dollar appears confident at the beginning of the week, and the reasons to expect its decline are diminishing.

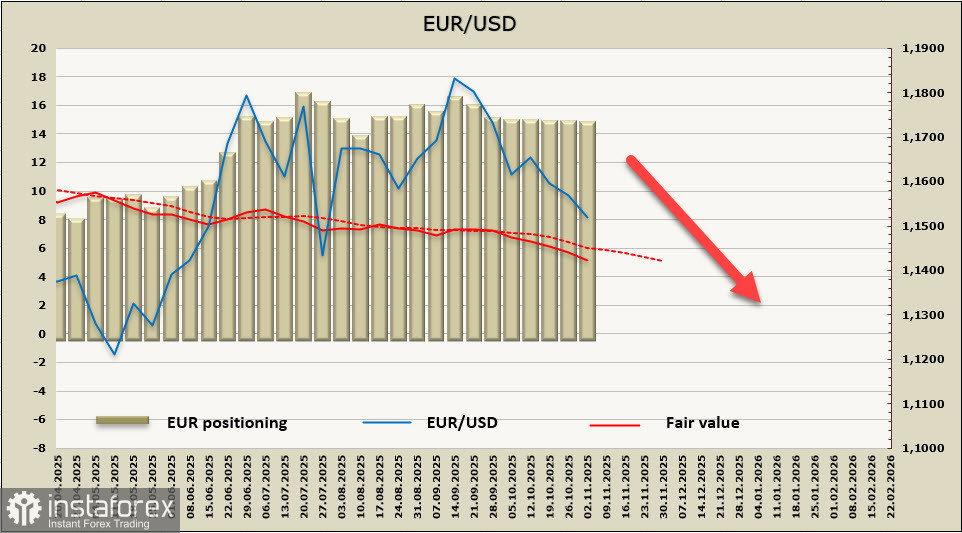

The calculated price is trending downward, and five weeks without CFTC data force reliance on incomplete data that does not favor the euro.

Last week, we anticipated a decline to 1.1540; support has been breached as the euro retreated to the technical level of 1.1506, which represents 23.6% of the rise from January to September. The support is weak, and the Federal Reserve's forecast revisions are putting pressure on the euro. We expect the decline to continue. The nearest target is 1.1390, followed by 1.1250, but further grounds are needed for confident declines.