English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Yesterday, equity indices closed with strong gains. The S&P 500 rose by 2.91%, while the Nasdaq 100 jumped by 3.83%. The Dow Jones Industrial Average strengthened by 2.49%.

Asian equity indices surged, recording the largest daily advance in the past twelve months. This optimistic spike coincided with continued gains in bonds, indicating reduced nervousness in financial markets. Market participants appear to be pricing in the possibility of a near-term end to the escalation in the Middle East conflict that earlier caused serious disruption and impaired global energy supplies.

A recent statement by US President Donald Trump, in which he forecast a potential end to the military confrontation with Iran within the next two to three weeks, served as the primary catalyst for this positive sentiment. Widely circulated, that information prompted the market to revise expectations downward for further geopolitical escalation and its economic fallout.

An assumed resolution of the Middle East conflict is critical to stabilizing energy prices, which are a key component of inflationary pressure. Reduced risks to oil and gas supplies could help ease inflation and create more favorable conditions for economic growth. That, in turn, supports equity markets by stimulating investment activity and lifting index levels.

Nevertheless, amid ongoing uncertainty about the war and the status of the Strait of Hormuz, oil has partially retraced Tuesday's losses and approached $105 per barrel. A resolution would likely restore investor confidence after five weeks of turbulence in energy and equity markets, during which some indices moved into correction territory. Attention will also focus on policymakers' responses to rising energy prices and supply disruptions and on whether slowing growth will affect corporate earnings at month-end.

According to JPMorgan Asset Management, the prospect of de-escalation from the US side could support risktaking in the near term. However, if the Trump administration revises its military strategy, the market could still face bouts of volatility.

In other market segments, gold rose for a fourth consecutive day, trading around $4,670 an ounce. Despite the recent rebound, March's nearly 12% drop in gold marked its worst monthly performance since October 2008.

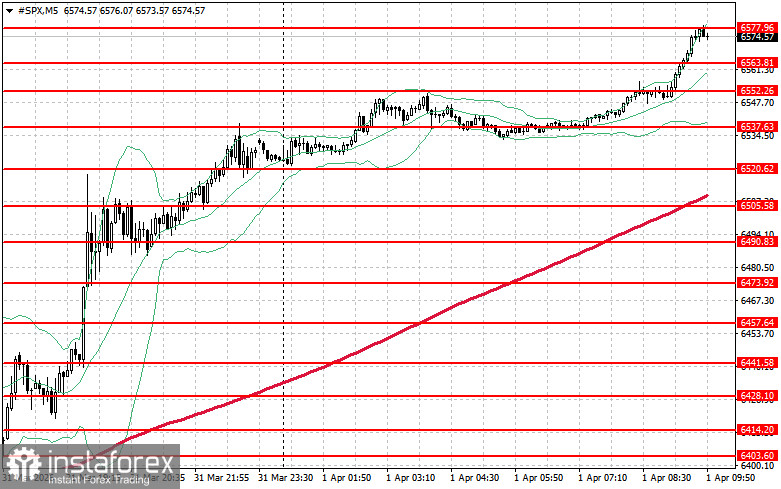

As for the technical picture of the S&P 500, the primary task for buyers today will be to overcome the nearest resistance level of $6,577. That would help the index gain upside momentum and could also pave the way for a thrust to $6,590. Equally a priority for bulls will be control above $6,603, which would strengthen buyers' positions. In the event of a downside move amid reduced risk appetite, buyers must assert themselves around $6,563. A break below that level would quickly push the instrument back to $6,552 and open the way to $6,537.