English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

Fundamental Background: The Paradox of the Strait of Hormuz and the Hawkish Fed Turnaround

Gold finds itself in a paradoxical situation. The geopolitical tension that historically should have supported this "safe haven" is working against the precious metal under current conditions. The key factor remains the linkage: escalation of the conflict in the Strait of Hormuz, rising oil prices, increased inflation expectations, tightening rhetoric from the Fed, rising bond yields and strengthening dollar, putting pressure on gold.

On the one hand, optimism regarding the negotiations persists. U.S. President Donald Trump stated that negotiations with Iran are "going well," and Secretary of State Marco Rubio noted that it may take "a few days" to conclude a deal.

On the other hand, on Monday, U.S. Central Command confirmed that it conducted "defensive strikes" in southern Iran, targeting missile installations and Iranian boats that were attempting to lay mines. Iran, in turn, reported that an American MQ-9 Reaper drone was shot down. These events diminish hopes for an immediate peace agreement and support demand for the dollar as a "safe haven."

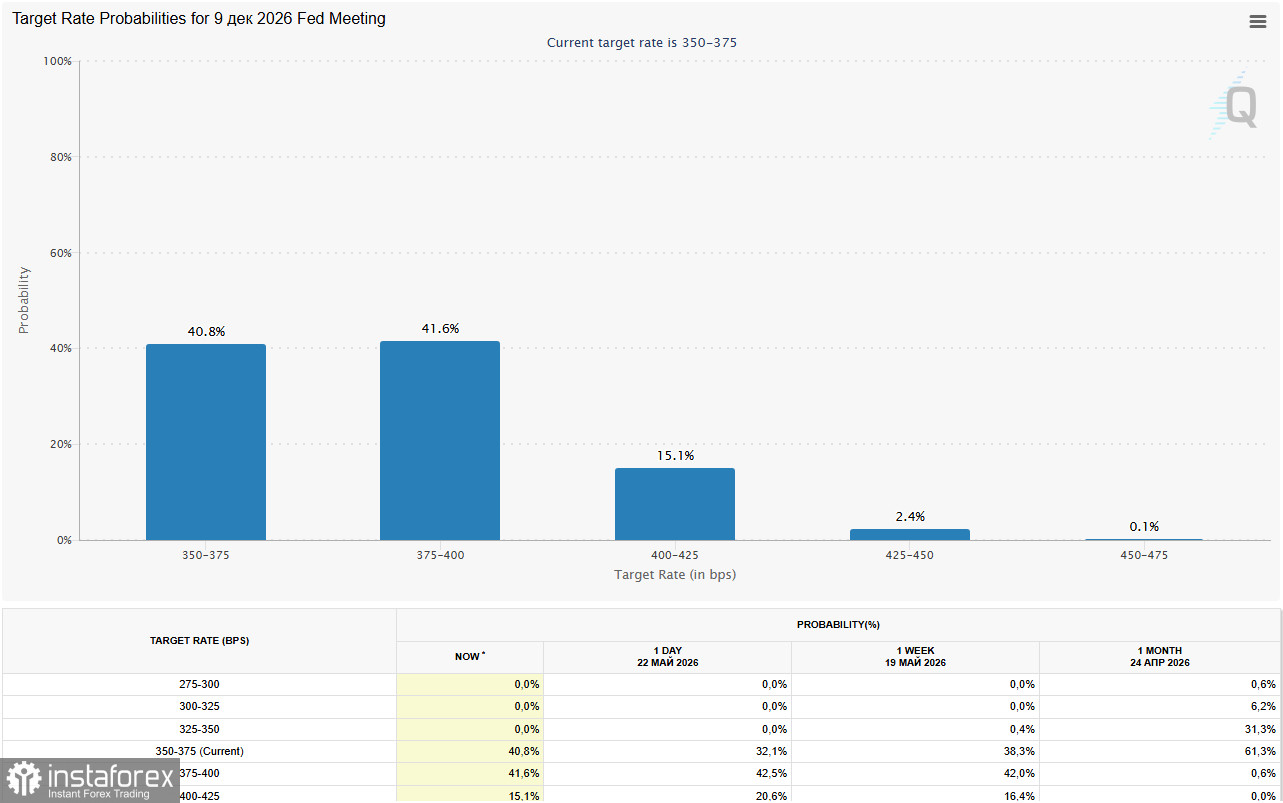

The main driver of pressure remains the reassessment of expectations regarding the Fed's monetary policy. The April data on CPI (3.8% year-on-year) and PPI (6.0% year-on-year) shocked the markets. According to the CME FedWatch tool, markets are pricing in about a 55% probability of a 25-basis-point rate hike by the end of 2026. Some economists expect the FOMC to abandon its "dovish tone" at the June meeting, noting that high yields on 10-year bonds increase the opportunity cost of holding gold, putting direct pressure on gold prices.

Meanwhile, as noted by the World Gold Council (WGC), investors and central banks are buying gold, ignoring record prices.

In the first quarter of 2026, the global gold market demonstrated unprecedented activity. According to the same WGC, global demand reached 1,231 tons, and its total value, including over-the-counter transactions, soared to a record $193 billion. The main drivers of this rally were investors seeking protection from inflation and central banks diversifying their reserves amid geopolitical tensions.

Key Drivers of Demand

- Investment Boom: Protection Against RisksDemand for investment gold (bars and coins) reached one of the highest quarterly results in history, standing at 474 tons. Investors worldwide, especially in Asia, actively bought the precious metal, anticipating interest rate cuts and seeking to hedge their capital against inflation and geopolitical risks. Inflows into gold-backed ETFs also continued, though at a more moderate pace than last year.

- Central Banks: Strategic PurchasesGlobal central banks remain net buyers of gold, acquiring 244 tons in the quarter. This trend is driven by a desire to reduce dependence on the U.S. dollar and strengthen financial stability amid uncertainty. Economists forecast that by the end of the year, central bank purchases could range from 640 to 850 tons.

- Technological Sector: Subtle but Steady GrowthDemand from the tech sector increased by 1% to 82 tons. The main driver here was the boom in AI infrastructure development and consumer electronics, where gold is essential for creating reliable connections.

- Jewelry Market: Under Price PressureHigh gold prices have curtailed demand from jewelry buyers—the volume of sales, measured in physical terms, fell by 23%. However, paradoxically, jewelry sales increased by 31%, indicating consumers' willingness to pay more. The markets of Asia and the Middle East showed the greatest resilience.

Key Events

| Date | Event | Expected Impact |

|---|---|---|

Thursday, May 28 (12:30 GMT) | Core PCE Index (Inflation) data for April in the U.S. | Key trigger—forecast 0.3% month-on-month, 3.3% year-on-year; a rise above this will strengthen the dollar and pressure gold. |

| Thursday, May 28 (12:30 GMT) | Second estimate of U.S. GDP for Q1 | Forecast: +2.3%; strong data will support the dollar. |

Weekend | Ongoing U.S.-Iran negotiations | Main geopolitical trigger—signing of a deal or a new escalation. |

Main Scenario

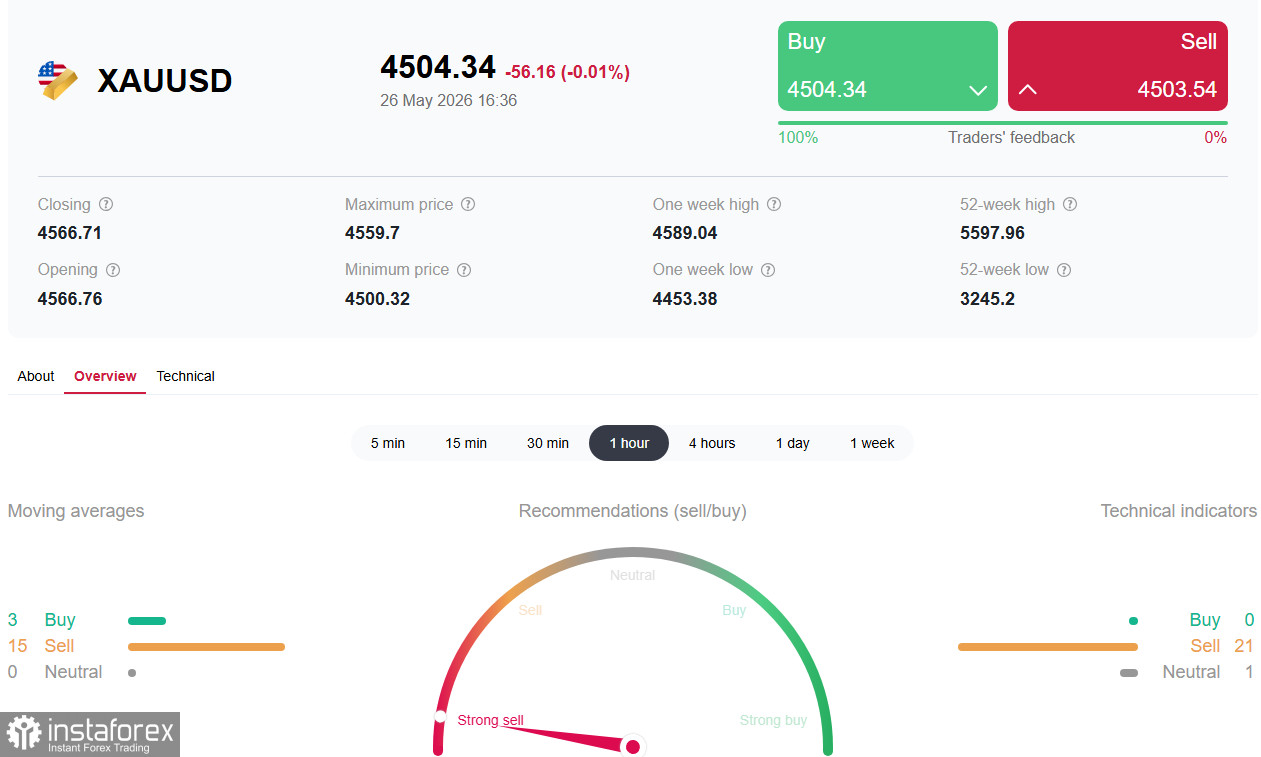

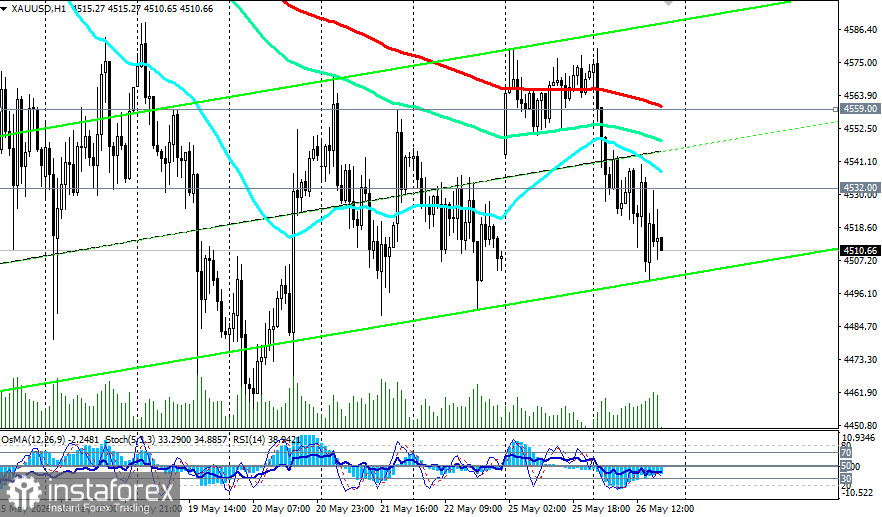

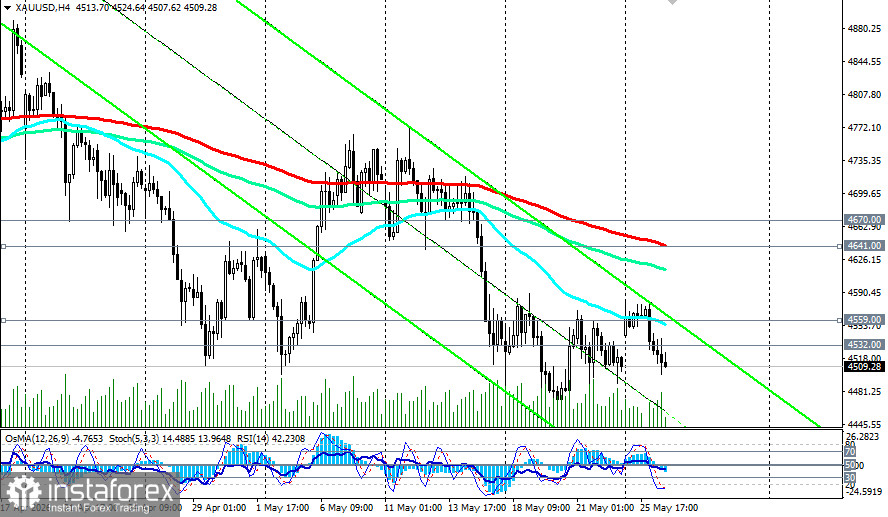

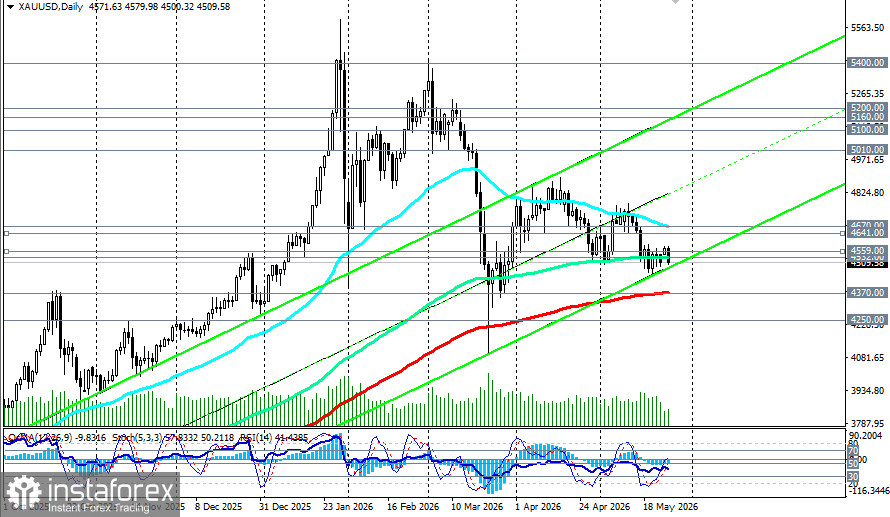

The main expectation is for a continued downward movement. A confident break and consolidation below the key support at $4,500.00 will open the way to $4,450.00 and then to the range of $4,400.00–$4,370.00 (200 EMA on the daily chart).

Key Conditions

- Data on the Core PCE in the U.S. strengthens hawkish expectations (over 3.3% year-on-year, 0.3%+ month-on-month).

- Lack of progress in U.S.-Iran negotiations (ongoing escalation or prolonged stalemate).

- The yield on 10-year Treasuries remains above 4.5%.

- Technical loss of support at 4500.00.

Conclusion

Gold is under powerful dual pressure. On one hand, the Fed's hawkish pivot (markets are pricing in more than a 50% probability of a rate increase by the end of the year) and ongoing geopolitical tensions create a bullish impulse for the dollar. On the other hand, structural demand from central banks (a 17% increase in the first quarter) and expectations of a medium-term de-escalation of the conflict provide support.

The key zone of 4500.00–4670.00 (50 EMA on the daily chart) will be the battleground in the coming days. As analysts in the precious metals market emphasize, as long as the conflict in the Strait of Hormuz remains unresolved and hawkish expectations from the Fed persist, the path of least resistance for gold is downward. Investors should closely monitor data on the Core PCE on Thursday, as it will determine whether the dollar gains additional momentum to assault the 4500.00 level and lower.

At the same time, in their 2026 forecasts, experts in the precious metals market agree that key factors for the gold market will remain geopolitics and inflation. Investment demand and central bank purchases are likely to keep rates high, supporting prices at elevated levels. Meanwhile, the jewelry sector will still face pressure, although resilient consumer spending may soften the decline. Under current conditions, gold continues to confirm its status as a key safe-haven asset in investors' portfolios.