English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

The EUR/USD pair remains within a local bearish impulse, although the bulls have gained some opportunities over the past two weeks. Last week, the international economic forum in Portugal took place, during which Kevin Warsh reaffirmed the need to bring inflation lower. This is an important development. However, Warsh did not clarify whether the Federal Reserve intends to achieve this through tighter monetary policy or whether it expects inflation to decline naturally as energy prices ease.

Since the market received no clear answer, it will continue to focus on inflation data. At the same time, the latest US labor market figures suggest that inflation is not the only factor policymakers should monitor. Job creation has once again remained relatively weak. Over the past three months, the economy has added approximately 100,000 fewer jobs than traders had expected. As a result, a slowing labor market may force the Federal Open Market Committee (FOMC) to weigh any decision on further monetary tightening much more carefully. The next inflation report should provide a clearer answer as to whether additional policy tightening—currently anticipated by most market participants—is justified.

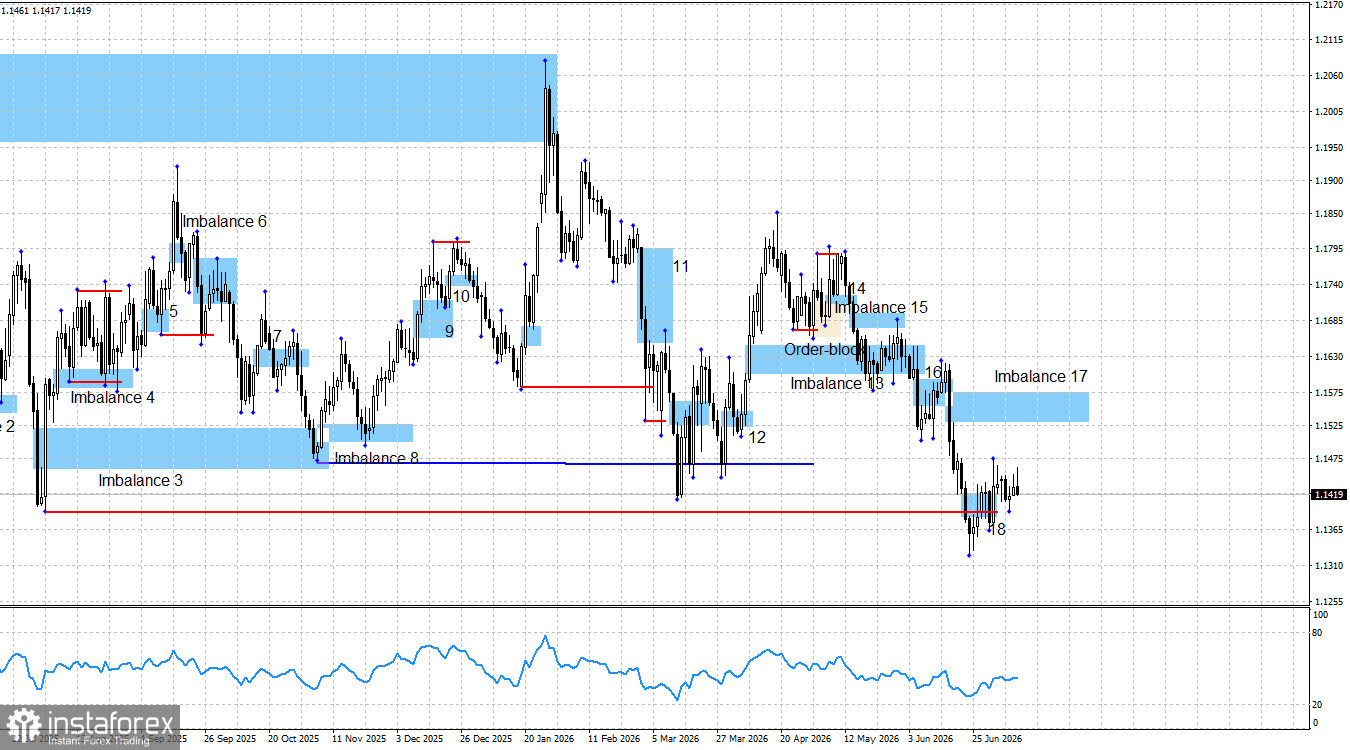

Over the past week and a half, the euro has managed only a modest recovery. This advance was sufficient to invalidate Imbalance No. 18, allowing traders to shift their focus toward Imbalance No. 17. As long as Imbalance No. 17 remains valid, the bearish impulse remains intact. However, over the past two weeks, the bulls have been unable to push the pair even 100 points higher. This week, the market has largely moved sideways.

In recent weeks, geopolitical developments have taken a back seat to Federal Reserve policy. This week, both Tehran and Washington once again violated the terms of the ceasefire and the agreement reached on June 17, but traders were hardly surprised. Donald Trump also signed an executive order revoking Iran's authorization to export oil, yet this development likewise had little impact on market sentiment.

The market did not react meaningfully to the end of the conflict, so it is equally unsurprising that it has shown little response to renewed tensions. We did not see the widely expected decline in the US dollar as geopolitical risks eased, nor did we see the euro strengthen in response to the European Central Bank's tighter monetary policy. The bears continued to dominate despite a fundamental and geopolitical backdrop that arguably favored the euro.

Now geopolitical developments are once again creating uncertainty, giving the bears a formal justification for renewed selling. In my view, however, traders are effectively pricing in events for the third time before they have actually occurred.

The current technical picture continues to indicate that the bearish impulse that began on April 17 remains in place. Bearish Imbalance No. 17 has not yet been mitigated, while Imbalance No. 18 was invalidated following weak US labor market data. No bullish technical patterns have formed, and none are likely to emerge over the next few days.

Therefore, the bulls may continue their corrective advance toward Imbalance No. 17, but there is currently no reliable technical setup to justify trading that move. It is also worth noting that liquidity has already been swept below the August 1 low from last year (marked by the red line on the chart). At present, this liquidity sweep remains the bulls' only meaningful technical support.

The economic calendar on Friday was virtually empty. There were no major releases apart from Germany's inflation data. The second estimate matched the preliminary reading exactly, confirming a slowdown in annual inflation to 2.4%.

The bulls still have numerous reasons to challenge the dollar in 2026, and the conflict in the Middle East has not materially changed that outlook. Structurally and from a long-term perspective, Donald Trump's policies—which contributed to the US dollar's significant decline last year—remain unchanged.

At present, I do not see any strong fundamental drivers supporting the US dollar despite the FOMC's hawkish rhetoric. Meanwhile, EUR/USD is approaching a series of important lows and swing points where liquidity could be swept. Such a move could provide the technical signal needed to reverse the current bearish impulse.

Economic Calendar for the United States and the Eurozone

The economic calendar for July 13 contains no scheduled events. Consequently, macroeconomic data is once again unlikely to influence market sentiment on Monday.

EUR/USD Forecast and Trading Outlook

In my view, the pair remains in the process of forming a longer-term bullish trend. Although the fundamental backdrop shifted sharply in favor of the bears four months ago, the broader uptrend cannot yet be considered invalidated or complete.

Therefore, the bulls may launch another advance after liquidity has been swept below the clearly defined lows. However, opening long positions at current levels is not advisable. It would be prudent to wait for bullish technical patterns to emerge first.

At present, traders are monitoring two bearish imbalances, one of which has already been invalidated. I would also highlight the proximity of four significant swing points where liquidity could be swept, together with the questionable fundamental justification for the US dollar's recent strength.

For this reason, I continue to expect a bullish recovery. However, I would prefer to see at least some technical confirmation of that scenario—or alternatively wait for a fresh sell signal to develop within Imbalance No. 17.